It’s either savings or selling as many interest-only terms expire

A new alarmist report has many believing that property Armageddon is nigh.

ME Bank’s bi-annual Household Financial Comfort Measures report surveyed 1500 households to gauge how they feel about their financial situation, including cost of living and household debt – and guess what they found?

More Australians are dipping into their savings to make ends meet as living expenses increase, wages stagnate, and mortgage and rental stress remain high.

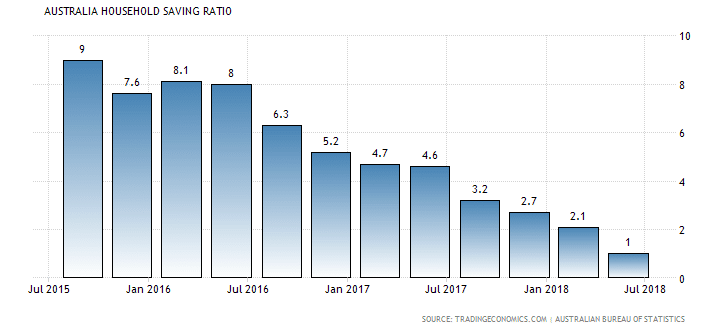

The report painted a grim picture with a quarter of Australian households reporting they had less than $1000 saved in the bank.

And this has been decreasing rapidly over the last 3 years as this graph suggests.

Plus, about 40 per cent spent all their income by the end of the week, down from 43 per cent six months ago, while 11 per cent overspent, up from eight per cent six months ago.

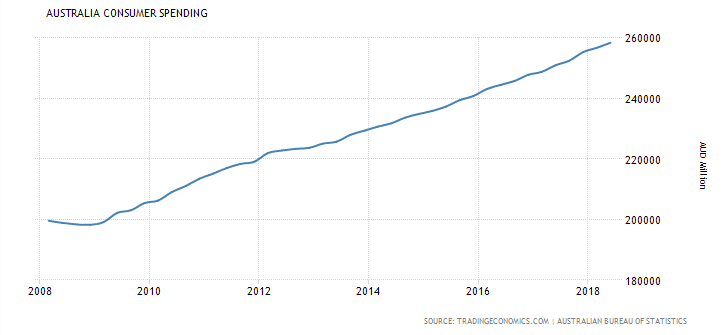

Our spending habits and rise in spending is highlighted here over the last 10 years.

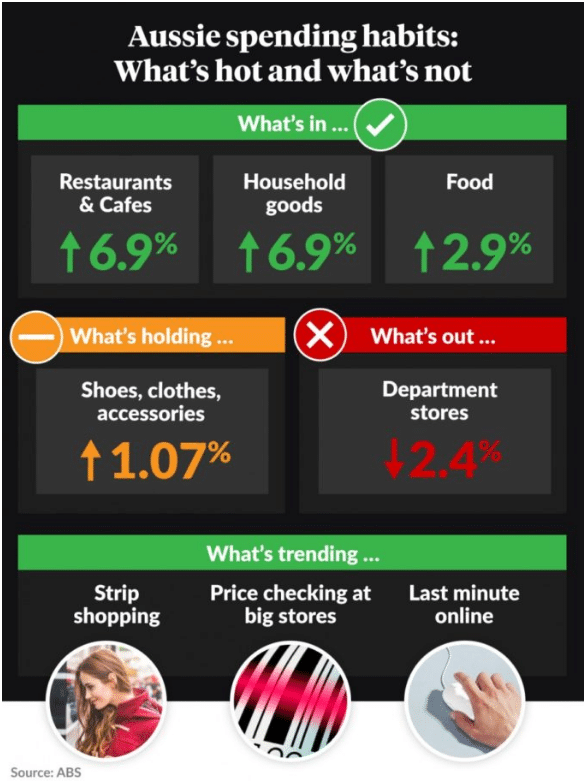

And our spending appears to be driven by our desire to socialise with a recent snapshot from the Australian Bureau of Statistics proving as much as this suggested here.

And it’s very interesting to analyse this further by looking at the spending habits of people in the different stages of life such as our singles, couples, then couples with kids and at their different stages of life.

One thing is clear, couples with teenage children seem to need a drink a lot more than the rest!

The ME bank survey also found 38 per cent of people were worried about their debt. This was significantly higher among Sydney residents (46 per cent) and those living in Melbourne (40 per cent).

And nearly 45 per cent of households were in mortgage stress, defined as spending more than 30 per cent of their income on their mortgage.

And this would seem to be with good measure.

So, what does it all mean?

The number one thing to understand in times of financial change, such as property prices dropping or interest only loan periods expiring, is not to panic.

Unfortunately, not many humans are able to do that – which is why we’ve had numerous black days on share markets over the past century.

There is no doubt that property prices in Sydney and parts of Melbourne are moderating, but as long as homebuyers and investors are in it for the long haul there is not much to worry about, of course, as long as you can afford it. And moderating prices aren’t the end of the world, they are actually are very normal part of every property cycle.

There is no doubt that property prices in Sydney and parts of Melbourne are moderating, but as long as homebuyers and investors are in it for the long haul there is not much to worry about, of course, as long as you can afford it. And moderating prices aren’t the end of the world, they are actually are very normal part of every property cycle.

If they are losing sleep over paying their mortgage repayments if interest rates increase marginally, well, perhaps they should never have applied for a loan that they clearly could not afford in the first place. I know, easier said than done as everyone wants “The Australian dream” but if it comes at the cost of your health, then is it really worth it?

Perhaps some people have interest-only loans because that was the only type of loan, at the time, that they could be approved for and now they’re worried about it changing to principal and interest repayments.

Again, a professional mortgage broker would probably not have agreed to source such a loan for them because they clearly wouldn’t be able to afford higher repayments when the interest only period expired. It is sad that both banks and brokers have actually put clients “at risk” by selling them into interest only loans because that’s all they could afford.

However, in slower market conditions, it would be preferable to refinance to another lender to secure another interest only loan rather than sell and potentially realise a loss.

Negative moment in time

Some homebuyers and investors might be sitting on a negative equity position because of moderating property prices in Sydney and Melbourne predominantly.

What this means is that their mortgage is greater than the price that they could potentially achieve for the property if they sold it.

Again, it’s vital to understand that moderation is a normal part of a market cycle, so the smart thing to do is to ride it out.

If someone has serious concerns about meeting their repayments, then it would be better to refinance than sell in the current market because they will likely end up losing their original deposit, buying costs and much more.

There’s a famous wealth creation saying that you should buy assets such as real estate or shares when others are fearful because you can usually get it for a discount. It was the doyen of investing – Warren Buffet – that said “Be Fearful when others are greedy and greedy when others are fearful.”

Clearly, that’s a sound strategy for savvy investors, but conversely it depends on sellers who give in to the fear of the unknown and probably pay a steep financial price for it.

The property market downturn, or let’s call it more a correction, in Sydney and Melbourne is now well entrenched, but it is just a moment in time.

Admittedly, confidence is also not high because of the recent political shenanigans in Canberra, but that also is not a reason to sell up and escape to the country.

Successful property investment has always been about ignoring the short-term and concentrating on the long-term, which has historically produced great results for those homebuyers and investors who could hold their nerve.

The information provided in this article is general in nature and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information with regard to your objectives, financial situation and needs.

with clients all over Australia and around the world. Andrew has over 30 year’s experience in the finance industry and has assisted clients to secure over $2 Billion in mortgage lending over his time. Intuitive Finance deals with all aspects of lending from helping first homebuyers, someone wanting to upgrade their home or starting out and experienced investors looking to secure that next investment property, we can assist with all those requirements. We also specialise in working with self-employed clients and getting them the best outcomes, along with Commercial and Asset finance solutions. Intuitive Finance is highly regarded in the industry and has been recognised as a national winner of the MFAA customer service award and also one of the finance industry’s top mortgage employers. Our brokers also feature regularly in the Top 100 mortgage brokers list in Australia.

- Choosing the right mortgage solution of variable fixed or both - October 8, 2024

- All You Need to Know About Bank Valuations - September 20, 2024

- Getting the Most out of the Spring Property Season - August 26, 2024